Value

- Base

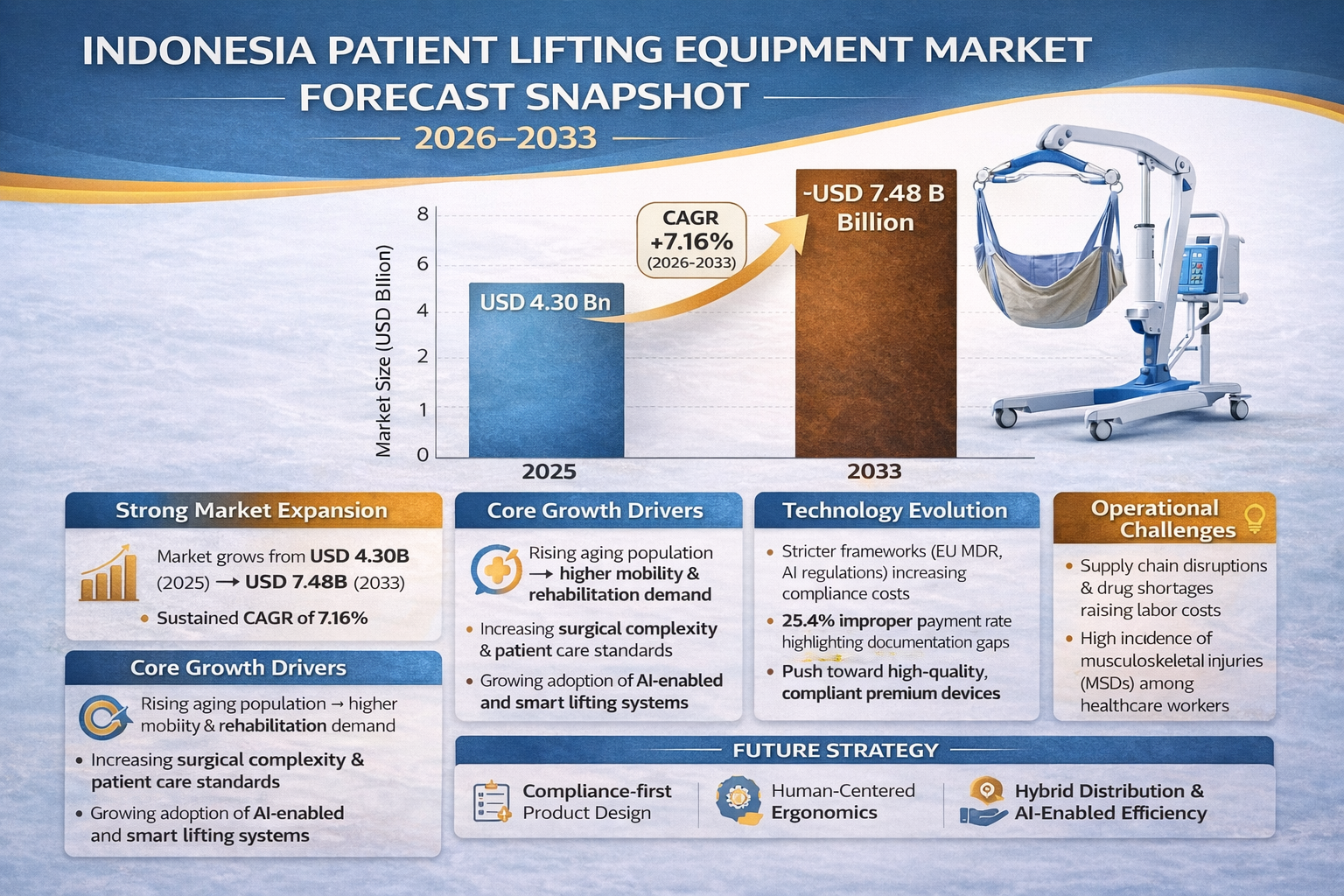

- 4.30

- Cagr

- 7.16

- Currency

- USD

- Forecast

- 7.48

- Unit

- Billion

Graph-backed node

The Patient Lifting Equipment market is characterized by a fragmented competitive landscape with moderate intensity, where two tier-1 players coexist alongside numerous smaller providers and niche specialists. Major healthcare systems like Mayo Clinic and Kaiser Permanente exemplify early adopters of advanced patient handling technologies, including human-centered design (HCD) adaptations and active exoskeletons such as ALDAK, developed by GOGOA, which can assist caregivers in lifting weights up to 40 kg. These innovations address critical occupational health risks, particularly musculoskeletal disorders (MSDs), which remain disproportionately high among healthcare workers, with incidence rates for nursing assistants measured at 166.3 per 10,000 workers—more than five times the average for all industries. The market’s operational model is predominantly hybrid, integrating both direct manufacturer sales and medical equipment distributors, supported by a growing online sales channel. Supply chain complexity is moderate but increasingly strained by drug shortages and medication supply disruptions, which indirectly impact patient handling through increased labor demands and operational costs. These bottlenecks compel healthcare providers to reassess procurement strategies, emphasizing reliability and patient-centered design in equipment selection. Regulatory oversight is intensifying, driven by evolving frameworks such as the European Union’s Regulations (EU) 2017/745 and 2017/746 on medical devices and in vitro diagnostics, alongside the newly enacted Regulation (EU) 2024/1689 addressing artificial intelligence in medical contexts. These regulations elevate compliance requirements related to safety, efficacy, and post-market surveillance, thereby raising market entry and operational execution standards. The introduction of centralized information hubs like the European Database on Medical Devices (EUDAMED), expected by 2027, will further enhance transparency and traceability. Investment trends display rising capital intensity, with healthcare facilities prioritizing projects that cover the weighted average cost of capital (WACC). Average Series A and C funding rounds in healthcare technology have increased, indicating maturation and investor confidence in innovative patient lifting solutions. Notably, large investments such as Target’s $550 million infusion into logistics infrastructure exemplify the capital scale necessary for scaling distribution and deployment capabilities.

The Patient Lifting Equipment market is characterized by a fragmented competitive landscape with moderate intensity, where two tier-1 players coexist alongside numerous smaller providers and niche specialists. Major healthcare systems like Mayo Clinic and Kaiser Permanente exemplify early adopters of advanced patient handling technologies, including human-centered design (HCD) adaptations and active exoskeletons such as ALDAK, developed by GOGOA, which can assist caregivers in lifting weights up to 40 kg. These innovations address critical occupational health risks, particularly musculoskeletal disorders (MSDs), which remain disproportionately high among healthcare workers, with incidence rates for nursing assistants measured at 166.3 per 10,000 workers—more than five times the average for all industries. The market’s operational model is predominantly hybrid, integrating both direct manufacturer sales and medical equipment distributors, supported by a growing online sales channel. Supply chain complexity is moderate but increasingly strained by drug shortages and medication supply disruptions, which indirectly impact patient handling through increased labor demands and operational costs. These bottlenecks compel healthcare providers to reassess procurement strategies, emphasizing reliability and patient-centered design in equipment selection. Regulatory oversight is intensifying, driven by evolving frameworks such as the European Union’s Regulations (EU) 2017/745 and 2017/746 on medical devices and in vitro diagnostics, alongside the newly enacted Regulation (EU) 2024/1689 addressing artificial intelligence in medical contexts. These regulations elevate compliance requirements related to safety, efficacy, and post-market surveillance, thereby raising market entry and operational execution standards. The introduction of centralized information hubs like the European Database on Medical Devices (EUDAMED), expected by 2027, will further enhance transparency and traceability. Investment trends display rising capital intensity, with healthcare facilities prioritizing projects that cover the weighted average cost of capital (WACC). Average Series A and C funding rounds in healthcare technology have increased, indicating maturation and investor confidence in innovative patient lifting solutions. Notably, large investments such as Target’s $550 million infusion into logistics infrastructure exemplify the capital scale necessary for scaling distribution and deployment capabilities.

The market size of Patient Lifting Equipment in 2025 is USD 4.30 billion.

The forecasted market size for Patient Lifting Equipment by 2033 is USD 7.48 billion.

The compound annual growth rate (CAGR) for the Patient Lifting Equipment market is 7.16%.

Key drivers of growth include increasing complexity of surgical procedures, demand for mobility support, and advancements in lifting technologies.

Environment: live

Freshness: 2026-06-12T19:44:36+00:00

Resolved node: MIMR-node_746de8b

Statsfocus

https://statsfocus.com

Knowledge graph of market intelligence